VA loans are an excellent option for Vets (and surviving spouses) who want to buy a home. The good news is that you can shop for a VA lender without having a VA loan certificate in hand.But if you’re serious about buying a home?You’ll need a VA home loan Certificate of Eligibility.Luckily, it isn’t rocket science.It’s pretty easy to get if you know what you’re doing.

And one thing is for sure.Here at the Wendy Thompson Lending Team, we know what we’re doing.We’re in the business of helping Vets make their dream of homeownership come true. Here’s what you need to know to get your VA loan certificate.

WHAT IS A VA LOAN CERTIFICATE OF ELIGIBILITY?

VA loans are exclusive to veterans. They have several benefits you won’t find with other home lending products, such as 0% down and lower income requirements.

But there’s a catch.

Before getting a loan, the lender must have proof you qualify.

That’s where the VA home loan certificate comes in.

Officially called a Certificate of Eligibility (COE), it’s a document that shows your lender you meet the requirements to get a VA home loan.

WHAT IS A VA LOAN CERTIFICATE OF ELIGIBILITY?

VA loans are exclusive to veterans. They have several benefits you won’t find with other home lending products, such as 0% down and lower income requirements.

But there’s a catch.

Before getting a loan, the lender must have proof you qualify.

That’s where the VA home loan certificate comes in.

Officially called a Certificate of Eligibility (COE), it’s a document that shows your lender you meet the requirements to get a VA home loan.

VA LOAN ELIGIBILITY

Because VA loans aren’t offered to just anyone, there’s criteria you need to meet.

But here’s the thing.

If you are a man or woman who served in the armed forces, you’ll likely have no trouble getting a COE.

Generally, if you served…

- In regular service for 2 years

- As a Reservist or in the National Guard for 6 years

- 90 days active duty during wartime

- Active duty during peacetime for 181 days

… then you’re eligible for a VA loan.

I can hear you now.

What if I don’t meet the minimum service requirements?

Learn More – Veterans Who Don’t Shop Around Pay Higher VA Mortgage Rates!

You might get a COE if you were discharged for hardship, reduction in force, or a few other reasons.

There’s just one situation where you might not qualify for a VA home loan certificate.

And that’s if you got an other than honorable, bad conduct, or dishonorable discharge.

If that’s the case, you still have options.

You can always apply for a discharge upgrade. If it goes through? You could be well on your way to getting VA benefits.

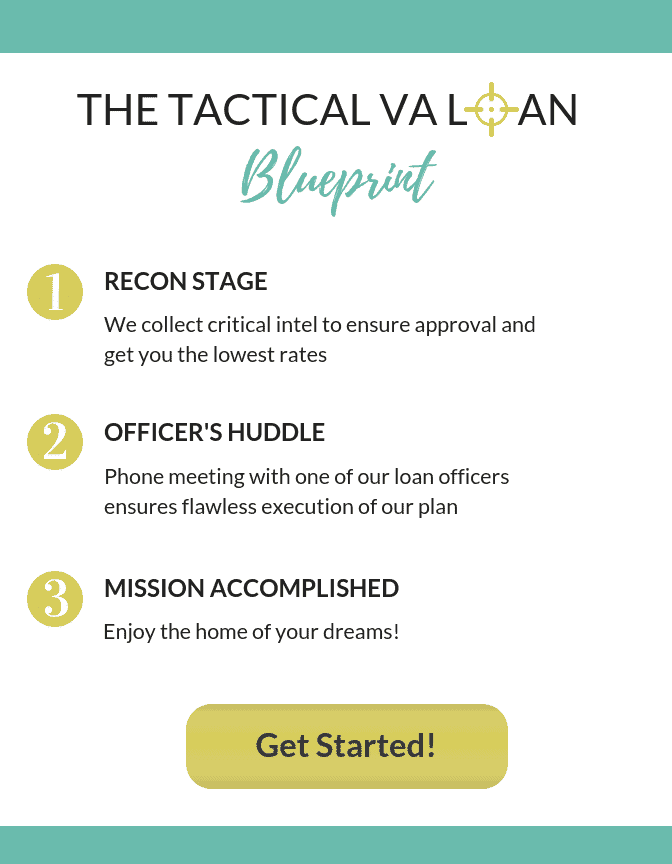

DO THIS BEFORE YOU APPLY

You can shop lenders before you apply for a COE. The secret is to pick a reputable lender.

Otherwise, you could set yourself up for disappointment.

You see, not every VA lender knows what they’re doing.

Two great options for a VA loan are USAA and Navy Federal.

But the Wendy Thompson Lending Team?

We’re a top-ranked VA Loan and Mortgage Specialist. And we’ve got you covered.

That’s why we’re giving you the inside scoop about what you need to apply for your COE.

Here’s what you’ll need if you’re a:

- Veteran: Discharge or separation papers (DD214)

- Service member: Signed statement of service

For National Guard or Reserve members, it depends on your status.

If you’re a current or former member, you might need:

- Discharge or separation papers (DD214)

- Signed statement of service

- NGB Form 22 and NGB Form 23

- Annual retirement points and proof of honorable service

Surviving spouses can qualify, too.

The requirements to apply for a VA loan certificate are different based on whether your spouse was a Veteran who died on active duty or had a service-connected disability.

Wherever you’re at on your journey as a Vet (or the spouse of a Vet!), we can help.

Reach out to the Wendy Thompson Lending Team, and we’ll get you on the path to homeownership.

APPLYING FOR VA HOME LOAN CERTIFICATE

Often, the hardest part of applying for a COE is getting the paperwork together.

After that’s done, the rest is a piece of cake.

The easiest way to get a VA certificate is to ask your lender. You can also apply online through the eBenefits portal or print this form to apply by mail.

The downside?

It could take up to six weeks to process.

Of course, you could get it much faster if you apply through your lender or using the eBenefits portal.

But your COE never expires. Once you have it in hand, you can take as long as you’d like to find a house to buy.

Amazing, isn’t it?

NEXT STEPS TO GET A VA LOAN

Your VA loan eligibility starts with knowing the answer to one question:

How much can I borrow?

You can use a VA mortgage calculator to know for sure. Just keep in mind it might not factor in your VA loan with funding fee, so make sure to add that in your final costs.

But here’s the deal.

No matter what you can afford, you deserve the very best service to help you get your dream home.

If you’re ready to move forward with a VA loan, don’t wait to contact us.

We’re here to help you every step of the way.