Getting a VA loan is a fantastic option for military members and their families. Picking a lender to work with is a crucial step. In fact, it’s the most important decision you’ll make.

Two of the best options to consider are USAA vs Navy Federal for VA loans.

Is one right for you?

Here at the Wendy Thompson Lending Team, we know what it takes to get you into a new home. That’s why we’re looking at both options to give you a rundown of the eligibility requirements, costs, service, and alternatives.

No tricks. No empty promises. We’re only interested in the facts.

Let’s go!

Who Can Use USAA Bank

Even though the U.S. Department of Veterans Affairs backs VA home loans, you must get a loan through a private lender. USAA Bank is one of the top providers of VA loans.

Generally, USAA is open to active, retired, and separated veterans and their families. Here’s what that looks like:

- Active servicemember

- Retired servicemember

- Separated servicemember with “Honorable” discharge

But wait, there’s more!

Eligible family members include:

- Spouses

- Widows

- Widowers and un-remarried former spouses

- Biological and step-children

Who Can Use Navy Federal Credit Union

When comparing USAA vs Navy Federal for VA loans, remember that Navy Federal is a credit union, not a bank.

It’s an important distinction because credit unions are generally more exclusive with who can be a member and take advantage of the services.

However, the lender has more membership options that you might think and includes:

- Active Duty servicemember

- Delayed Entry Program (DEP)

- DoD Officer Candidate/ROTC

- DoD Reservists

- Veterans, retirees, and annuitants

But the best part?

Navy Federal is open to more immediate family members than USAA.

The credit union lists these family members as eligible:

- Parents

- Grandparents

- Spouses

- Siblings

- Biological, adopted, and step-children

- Grandchildren

- Household members

USAA Vs Navy Federal VA Funding Loan Amount

VA loans are great because you can usually get into a house without making a down payment.

There’s one catch: the funding fee.

But it’s a one-time thing, and you might qualify for an exemption.

So, how much is it?

Well, it depends on three things:

- How much you borrow

- How much you put down

- Your military status

The first two might not surprise you. But military status?

Yes, that’s right. Your VA funding military type is a factor that determines your funding fee.

But there is good news!

Your VA funding fee is the same no matter which lender you pick. What sets one lender apart from the next is the service you get.

Let’s talk about that now.

Veterans Who Don’t Shop Around Pay Higher VA Mortgage Rates

USAA Vs Navy Federal Service

When you’re buying a home, it all comes down to service.

Think about it…

The only thing standing between you and the house you want is getting the funding you need.

And if a lender drags their feet or gets something wrong?

It could mean missing out on your dream house!

You don’t want to become a member of USAA or Navy Federal only to discover it’s impossible to get in touch with a customer service rep.

Navy Federal Credit Union has representatives available around the clock, while USAA limits customer service hours to Monday through Friday, 8 a.m. to 5 p.m. CT.

But what about qualifying for a VA loan?

Let’s consider your credit score next.

USAA Vs Navy Federal Credit Score

I know what you’re thinking…

If the VA sets credit score requirements, why does it matter which lender I choose?

Here’s the thing:

The U.S. Department of Veterans Affairs doesn’t set minimum VA credit score requirements.

It’s up to the individual lender to set the bar on what credit score you need!

Generally, you must have at least a VA funding credit score of at least 640.

But each lender can set the bar higher or lower, depending on their internal policies. And that makes choosing the right lender even more important.

Lenders set their own interest rates, too. Though they try to stay competitive, you might get a higher (or lower!) rate if you go with USAA vs Navy Federal.

Alternatives To USAA And Navy Federal For VA Loans

USAA and Navy Federal are popular choices, but they aren’t the only options. Several lenders can help you get a VA mortgage for your next house, including:

- PenFed

- US Bank

- Loan Depot

- Veterans United

Just remember: they’re not all created equal.

Before you jump into a VA loan application, consider the lender’s costs, service, and interest rates.

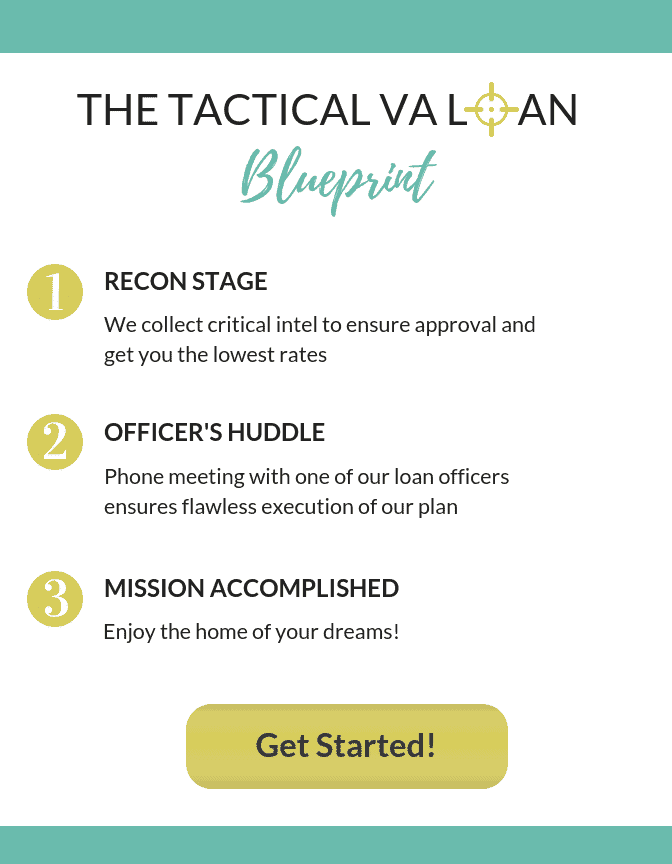

READY TO GET YOUR VA LOAN?

If you don’t have experience with the VA loan program, the process can seem confusing. Pick the wrong lender, and you could have a miserable experience.

But the right lender?

It makes all the difference.

That’s why there’s no need to worry when you work with the Wendy Thompson Lending Team!

We’re a top-ranked VA Loan and Mortgage specialist, and we know what it takes to get you into a new home.

Call us today! (901) 461-8858